Home >

Blog >

The economic fallout from theMiddle East (and the impact onproperty)

The economic fallout from theMiddle East (and the impact onproperty)

Posted

on 24 March 2026

Source: Ray White via Linkedin

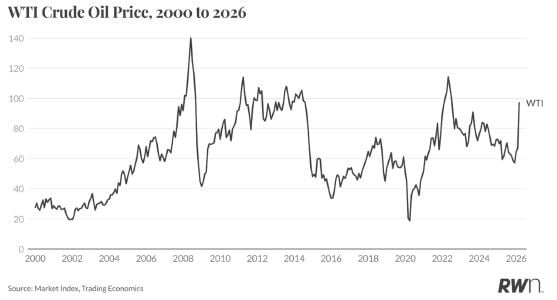

The economic fallout from the Middle East will not be evenly distributed across the global economy. Countries heavily reliant on imported energy,particularly across Europe and Asia, face the greatest risk as oil and gas prices rise. Australia sits in a more complex position. As a major exporter of LNG and coal, higher energy prices can lift national income and government revenues.

But Australia also imports most of the fuel used domestically, meaning global energy shocks quickly translate into higher petrol prices, rising business costs and renewed inflation pressures. The result is a split outcome across the economy, with clear winners among resource exporters but growing pressure on households, fuel-intensive industries and parts of the housing market.

Mining and energy exporters stand to gain. The clearest beneficiaries are Australia’s energy and resource exporters.When geopolitical tensions disrupt global energy markets, prices for oil,gas and often coal tend to rise. For Australia, this can translate into stronger export revenues and improved terms of trade.

Liquefied natural gas producers are particularly well positioned. LNG markets are highly sensitive to supply disruptions, and higher global prices can quickly boost revenue for Australian exporters supplying Asia and Europe. Coal exporters can also benefit as countries substitute away from expensive gas or seek alternative sources of energy.

Australia has seen this dynamic before. During the global financial crisis,the country avoided a recession in part because strong demand for resources, particularly from China, supported mining exports and national income even as other advanced economies contracted. While the drivers of the current shock are different, the mechanism is similar: when global commodity prices rise sharply, Australia’s resource sector provides an economic buffer.

Higher commodity prices also flow through to government finances.Resource-rich states such as Western Australia and Queensland receive significant royalty revenues from mining and energy production, meaning periods of elevated commodity prices can provide a fiscal windfall.Company tax receipts also rise when mining profits increase.

Households feel the immediate impact

The benefits to exporters contrast sharply with the experience of households. While Australia exports energy, it imports most of the refined petroleum products used domestically. That means global oil price increases quickly translate into higher petrol and diesel prices.

For households already facing elevated living costs, higher fuel prices act as an additional squeeze on budgets. Transport costs rise first, but the effects spread more broadly across the economy. Freight becomes more expensive, pushing up the cost of groceries and consumer goods. Airfares rise as airlines pass through higher jet fuel costs. Over time, the cumulative effect is reduced purchasing power and weaker household consumption.

These pressures are felt most strongly in outer suburban and regional areas where households rely more heavily on cars and where transport distances are longer.

Construction and housing face a complicated outlook

The housing sector sits at the centre of this dynamic. Energy shocks feed directly into construction costs. Building relies heavily on diesel-powered machinery, fuel-intensive transport and energy-heavy materials such as steel, cement and bricks. When fuel prices rise, the cost of delivering new housing rises with them.

Higher construction costs arrive at a time when the economics of development are already tight. If building becomes more expensive, fewer projects stack up financially and the pipeline of new housing slows.

At the same time, rising energy prices risk keeping inflation elevated across the broader economy. With this comes higher interest rates, which leads to slower price growth. It does, however, also make new housing harder to deliver. Rising financing costs reduce development feasibility,particularly for higher-density projects where debt plays a larger role in funding construction.

The result is a complicated picture for the housing market. Price growth is likely to slow as borrowing capacity tightens, but the supply response could weaken at the same time. When fewer homes are built, the underlying shortage of housing deepens.

In practice, this often shifts pressure into the rental market. With population growth continuing and new supply limited, rents remain elevated even when house price growth moderates, which is a further complication for the inflation outlook.