Home >

Blog >

Navigating the Rise of AI in Valuation: Opportunities, Risks, and Standards

Navigating the Rise of AI in Valuation: Opportunities, Risks, and Standards

Posted

on 2 September 2025

Source: IVSC

Introduction

Although technology has been used in valuations for decades, recent advances may profoundly affect how valuations are performed and reported.

The IVSC recognises that technology continues to evolve and is increasingly influencing valuation practice. As with all developments that have the potential to shape or impact the valuation profession, the IVSC actively monitors advancements in this area. Our commitment remains to support professional valuers by helping them navigate change, including the effective and appropriate use of technology within a robust, principles based valuation framework. The IVSC does not support the replacement of professional valuers and continues to uphold the critical role of human judgement, scepticism, and accountability in the valuation process.

The IVSC has noted the following areas in which there have been significant changes in valuations include:

Sourcing and interpreting data, including images and other unstructured data

Calculating, including models and predictive analytics, enquiring, reporting, and presenting

Some well-known AI LLMs capable of all the above, to one degree or another, include: OpenAI's ChatGPT, Anthropic's Claude, Microsoft's Copilot, Deepseek AI's Deepseek, Google DeepMind's Gemini, and xAI's Grok, as well as many proprietary machine learning-based AI systems.

This is a perspectives paper that describes:

How the IVSC perceives recent technology impacting valuations

Opportunities and threats to valuations posed by these technologies

How current IVS standards address the potential impact to valuations

Potential areas for the IVSC to enhance its standards to further address these new technologies

In addition, this perspective paper solicits feedback from stakeholders to understand future standard setting needs.

IVS (effective 31 January 2025) and Valuation Technology

In recognition of recent significant technological advances, the recently published IVS (effective 31 January 2025) includes requirements on governance, data and inputs, valuation models and quality controls.

Furthermore, the Glossary includes the following definitions for an Automated Valuation Model and for a Valuation Model1:

Automated Valuation Model (AVM): A type of model that provides an automated calculation for a specified asset at a specified date, using an algorithm or other calculation techniques without the valuer applying professional judgement over the model, including assessing, and selecting inputs or reviewing outputs

Valuation Model: A quantitative implementation of a method in whole or in part that converts inputs into outputs used in the development of a value

Moreover, IVS 100 Valuation Framework now includes a section on the use of a specialist or service organisation to recognise that where a valuer does not possess the necessary knowledge, skills, experience, or data to perform all aspects of a valuation,

they may seek assistance from these parties provided this is agreed and disclosed in the scope of work. This is particularly relevant for data sourcing and processing and for the provision of valuation models.

IVS (effective 31 January 2025) also includes the following new standards in respect of data and inputs and valuation models:

IVS 104 Data and Inputs

IVS 105 Valuation Models

IVS 104 Data and Inputs sets out requirements over the selection and use of data to be used as inputs in the valuation. The aim of the valuation is to maximise the use of relevant and observable data to the degree that it is possible. IVS 104 provides

further standards on the use of a specialist or service organisation, characteristics of relevant data, input selection and data and input documentation. It should be noted that this chapter further states that “the valuer is responsible for assessing and selecting the data, assumptions and adjustments to be used as inputs in the valuation based upon professional judgement and professional scepticism.”

IVS 105 Valuation Models addresses the selection and use of valuation models to be used in the valuation process. IVS 105 provides further standards on the use of a specialist or service organisation, characteristics of appropriate valuation

models and valuation model selection and use.

IVS 105 further states that “valuation models can be developed internally or sourced externally from a specialist or service organisation,” but “in all cases the valuer must apply professional judgement and professional scepticism in the selection and

use of valuation models and the application of inputs used in the valuation model.”

Moreover, IVS states that “no model without the valuer applying professional judgement, for example an automated valuation model (AVM), can produce an IVS-compliant valuation.”

At this point in time a valuation model, including one which uses artificial intelligence, machine learning or deep learning cannot produce an IVS compliant valuation without the valuer’s professional judgement as in addition to many other standards contained within IVS (effective 31 January 2025) it would not meet the following requirements contained within IVS 105 in relation to valuation model selection and use:

“40.02 Regardless of whether the valuation model is developed internally or externally sourced the valuer must assess the valuation model in order to determine that the valuation model is fit for its intended use.

40.03 The valuer must understand the way the valuation model operates.”

It should be noted that, this does not mean that a valuation model which uses artificial intelligence, machine learning or deep learning cannot be used as a tool to assist the valuer in their valuation work. The valuer must understand the design and

implementation of the valuation model and its limitations and must be able to use professional judgement to determine the appropriateness of components relied upon in the valuation.

In fact, the IVSC Technical Boards have noted the increasing use of technology in valuation, for part of or the whole of determining a value or developing the valuation report.

Examples of the former include the use of advance data collection and valuation models in commonly used applications provided by service organisations such as Bloomberg or Capital IQ or the use of software for valuation modelling or

reporting, which may have some form of AI embedded within their systems. It should be noted that under IVS “if significant inputs are inadequate or cannot be sufficiently justified, the valuation would not comply with IVS2.”

The IVSC Standards Review Board (SRB) recognises that this is a fast-developing field, and the situation may change in future editions of the IVS due to additional development in the fields of artificial intelligence, machine learning and deep

learning.

Opportunities and Risks

Artificial Intelligence (AI) is currently being used by valuers, though the extent and use of AI across different markets and within markets may vary widely.

As stated in the CBVI Primer on Artificial Intelligence, there are two types of AI that are currently being used in financial services and litigation.

“Predictive AI is being used to analyse large datasets to forecast trends and identify patterns, to help professionals make informed decisions. It is also being used to identify potential risks and opportunities in the market.

Generative AI tools, such as ChatGPT, Copilot, Gemini, DALL-E, and Midjourney are being used to create original media such as text, images, video, or audio in response to prompts from users. These systems are often powered by large

language models (LLMs), which learn patterns from vast amounts of data.”

AI can assist the valuer through automating more straightforward valuation tasks, including report writing, and providing the valuer with the opportunity to focus on more critical valuation matters, where greater levels of professional judgement

and professional scepticism are required.

In the field of property valuation AVMs are increasingly used by banks in conjunction with valuation reports to make secured lending decisions on residential property.

IVS Valuation Process

Artificial intelligence can be applied at various stages of the IVS valuation process to help inform the opinion of value. However, its use presents both opportunities and risks, all of which must be carefully assessed and managed through the valuer’s professional judgement and professional scepticism.

IVS 100 Valuation Framework

AI and other forms of technology could be used to provide a useful tool within the valuation quality control process to ensure compliance with relevant monitoring and control procedures.

IVS 101 Scope of Work

AI and other forms of technology could be used in developing the scope of work through the use of automation and could also be used to check that all the relevant elements are contained within the scope of work.

IVS 102 Bases of Value

AI and other forms of technology could be used to review valuation reports to check that the correct basis of value has been used and to ensure there are no inconsistencies within the value reported.

IVS 103 Valuation Approaches

AI and other forms of valuation may have little impact on the valuation approaches used, which is within the professional judgment of the valuer. However, such use could influence the valuation methodology that is used as more complex methodologies using or integrating AI are developed. However, as illustrated below AI could play a key part in both the data provided and in the valuation model.

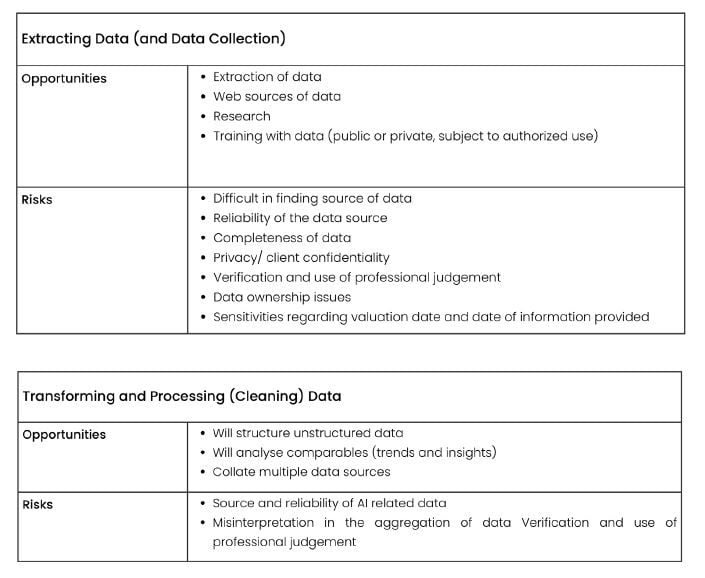

IVS 104 Data and Inputs

Many valuation providers are already using AI and other forms of technology to assist in extracting, transforming, and processing data. However, there are several opportunities and risks in relation to the use of technology for these purposes,

which are illustrated in the tables below. The opportunities and risk factors are not exhaustive. We must emphasise that data science has made huge progresses, which creates an opportunity to feed AI to make it even more efficient and reliable.

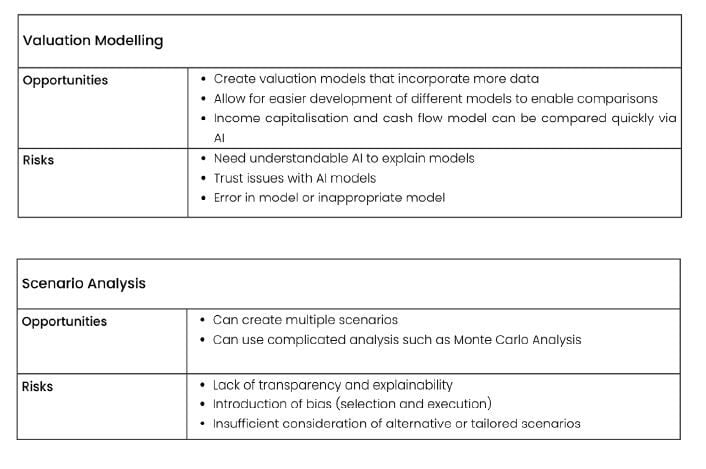

IVS 105 Valuation Models

The use of AI and other forms of technology for valuation models is still a developing field and can be subdivided into the use of technology for the valuation models themselves and for scenario analysis.

However, there are several opportunities and risks in relation to the use of technology for these purposes, which are illustrated in the tables below. The opportunities and risk factors are not exhaustive.

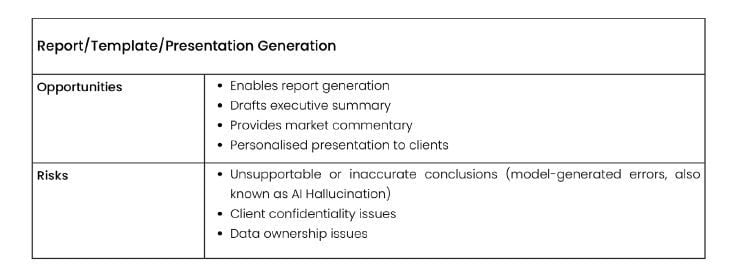

IVS 106 Documentation and Reporting

AI and other forms of technology are already frequently used by some valuers for assisting them in valuation report writing, either through the use of Chat GPT or other forms of publicly available AI for part of the valuation such as the market commentary. In other instances, the report writing may be a fully automated process within their firm.

However, there are several opportunities and risks in relation to the use of technology for these purposes, which are illustrated in the tables below. The opportunities and risk factors are not exhaustive.

When drafting a valuation report, it is essential for the valuer to maintain control over the content—ensuring the materiality and relevance of descriptions, verifying data sources, and confirming that all facts presented are unbiased, accurate, and

appropriate.

Possible Future

Enhancements to IVS

Even though, as stated above, the use of technology provides significant opportunities to improve valuation, it also presents challenges and risk within the following areas to which the IVSC Technical Boards are considering future

enhancements:

Transparency

Data and Inputs

Valuation Models and Systems

Quality Control

Transparency

At this point in time, IVSC is aware that a number of valuers are either knowingly or unknowingly using elements of AI within valuations or to assist them in report writing.

The IVSC Standard Review Board and its Technical Boards see transparency as an extremely important IVS general principle. This is a matter for the valuer when applying IVS 101 Scope of Work or within IVS 106 Documentation to state whether AI

will be used or has been used within the valuation process, and to include details in relation to what, why and how, if any, artificial intelligence has been used within the valuation process.

Data and Inputs

Ensuring the accuracy and reliability of data used within valuations is critical, particularly when future models may have the ability to not only source but also create the data that is used in models. IVS 104 states that:

“40.01 Inputs must be selected from relevant data in the context of the asset or liability being valued, the scope of work, the valuation method, and the valuation model.

40.02 Inputs must be sufficient for the valuation models being used to value the asset and/or liability based on the valuer using professional judgement.”

And further states that:

“50.01 The source, selection and use of significant data and inputs must be explained, justified, and documented. 50.02 Documentation must be sufficient to enable the valuer applying professional judgement to understand why specific

data was determined to be relevant and inputs were selected and were considered reasonable.”

As a result, the valuer will have to use means such as sampling, benchmarking,calibration, proxying and/or recalculation so the valuer can apply their professional judgement and professional scepticism to ensure that the data sample is sufficient

and that the inputs used are fit for purpose.

Furthermore, the use of open-source or, in some cases, closed-source AI without adequate safeguards may pose risks to client confidentiality. Without clear lines of separation, such use could breach data protection laws or inadvertently violate

non-disclosure agreements.

Increased cybersecurity may also be required to deal with evolving threats, complex networks, and the need for valuers to protect sensitive information.

Valuation Models and Systems

The valuer is required to understand and assess the valuation model and ensure that it is fit for purpose. IVS 105 states that:

“Regardless of whether the valuation model is developed internally or externally sourced the valuer must assess the valuation model in order to determine that the valuation model is fit for its intended use.”

And further states that:

“40.04 The valuation model should be tested for functionality and outputs must be analysed for accuracy. Any significant limitations should be identified, along with any potentially significant adjustments.

40.05 Valuation models used over time should be maintained, monitored, assessed, and adjusted to ensure that they remain appropriate, accurate and complete.”

This is especially challenging because some AI models are so complex that understanding them requires another model designed to translate their behaviour into human-understandable terms — a process known as Explainable AI.

As valuation models become more sophisticated, increased testing will be essential within the valuation process. Valuers will need to regularly ensure that models are functioning correctly through model development, model validation, and model monitoring. This can involve techniques such as benchmarking, time series analysis, performance monitoring, or independent valuations—all of which support the application of professional judgment and professional scepticism to confirm that the valuation model is fit for purpose.

The Canadian Office of the Superintendent of Financial Institutions (OSFI) states that:

“Explainability of model outputs enhances the ability to mitigate the risks and unintended outcomes associated with using them and supports model soundness and accountability.”

Furthermore, the valuer needs to ensure that there is no algorithmic bias, as illustrated in the UNESCO statement that:

“AI is not neutral: AI-based decisions are susceptible to inaccuracies, discriminatory outcomes, embedded or inserted bias.”

This highlights the risk of an inaccurate AI response (hallucinations), which is a critical concern for valuers seeking to avoid bias. As with any tool used to support valuation work, valuers must avoid "black box" situations by applying professional judgment and professional scepticism and maintaining full control throughout the whole valuation process.

Quality Control

In considering the increasing use of AI and deep learning within valuation, IVS may need to be revised to ensure that quality controls include review and challenge.

IVS 500 Financial Instruments already includes the following requirements in relation to the application of quality control:

“160.01 Quality controls must be designed and implemented to help ensure that valuations are performed in compliance with IVS.

160.02 To achieve this, quality controls should confirm as of the valuation date that quality control processes have ensured the following:

……(c) Quality control processes have been executed over:

(i) data, assumptions, adjustments, and inputs,

(ii) the selection of models to determine value,

(iii) manual or other interventions over the established process,

(iv) communication and documentation of the valuation process and the resultant value.”

In future iterations of IVS, similar requirements will have to be included within the General Standards to ensure that there is a sufficient degree of review and challenge throughout the valuation process.

Conclusion

Although valuations conducted solely using AI, automated statistical models, machine learning, or deep learning are not currently compliant with IVS standards, these technologies offer valuers meaningful opportunities to enhance the valuation

process. They can improve efficiency, expand data access, and support more robust analyses. However, their use also raises important questions about how valuers can consistently apply professional judgment and professional scepticism throughout the valuation process, while effectively managing valuation risk, which IVS defines as “the possibility that the value is not appropriate for its intended use.”