Source: Australian Property Journal

RATINGS agency Fitch is forecasting house prices will decline by 5-10% over the 12 to 18 months due to lower immigration but economists disagree and believe the housing downturn will soon come to an end and they predict values could rise by up to 15% in 2021.

Fitch noted that immigration was already slowing prior to the outbreak of the pandemic but numbers have plunged due to the government's stricter controls on international travel to combat the spread of COVID-19.

Immigration is expected fall by 15% in the year to June 2020 and another 85% in FY21, almost 200,000 fewer permanent arrivals compared to FY19, and mark the lowest level of net immigration since June 1993. Fitch said this reduction would imply demand for around 76,000 fewer dwellings than would have otherwise been the case and it estimates the population growth for Australia will reach just 0.7% in 2020, a level not seen in the past 40 years, and down from 1.4% in 2019.

Fitch structured finance managing director Ben McCarthy said the exceptional uncertainty related to the current recession, and its disproportionate impact on young people, is likely to reduce household formation and property demand even more.

"The Australian Bureau of Statistics has indicated that 171,000 housing approvals were granted in FY20. This is significantly down on the peak for approvals of 243,000 in the 12 months to August 2016, which may help to mitigate the demand shock. Monetary policy has also loosened, which could provide some support for house prices, as could government policies targeting support for the housing sector.

"Nevertheless, we believe house prices will face downward pressure nationwide, as supportive factors will be outweighed by the impact of the change in net immigration, along with high unemployment and general economic uncertainty. Indeed, risks to our forecast for house prices are skewed to the downside, and price falls could exceed 10% if our assumptions about the path of the pandemic prove to be overly optimistic," McCarthy said.

Fitch estimates that immigration into Australia has added approximately 1% to GDP annually over the past 10 years. McCarthy said an end to travel restrictions could result in a rapid reversion of immigration to previous trends, and new permanent arrivals will remain a driver of medium-term growth.

"However, we do not expect restrictions to be eased until well into 2021, and there may be public pressure on the authorities to limit immigration in the near term as long as unemployment remains high," he concluded.

Meanwhile Capital Economics has revised its forecast. Senior economist Marcel Thieliant said the current housing downturn will soon come to an end.

"We now expect house prices across the eight capital cities to fall by just 3% from their peak in April and to rise by 7% in 2021. House prices across the eight capital cities have fallen by a small 1.7% since their peak in April and there are already signs that prices have started to bottom out outside of Sydney and Melbourne.

"The RBA has cut interest rates from 7% to 0.25% and won't hike its policy rate anytime soon. Housing downturns usually end a few months after the RBA's starts cutting interest rates. The reduction in borrowing costs means that housing affordability is looking attractive. Indeed, it has already resulted in a marked pick-up in housing finance commitments, which points to rising house prices.

"Other leading indicators also suggest that the housing market is about to turn. Auction clearance rates have rebounded from just over 30% in April to nearly 60% in recent months, consistent with rising house prices. Admittedly, the low number of auctions suggests that we should put less emphasis on clearing rates than we would normally do. But other indicators tell a similar story. CoreLogic data on home sales show a strong rebound from the lockdown in April. And while there was a renewed weakening in August, our sales-to-listings ratio suggests that prices will soon start to rise again,"

But Thieliant warns there are several downside risks including lower immigration, weaker labour markets and the end of the HomeBuilder grant.

"It's possible that the labour market will weaken yet again as the JobKeeper wage subsidy is scaled back. What's more, the phasing out of mortgage deferrals may result in a wave of forced sales,"

Australian banks have deferred $176 billion in mortgages until September or October, equivalent to 9.7% of the outstanding stock and some customers may have to sell their house if they are unable to repay their loan over the longer term.

"The early 1990s recession provides some indication of the possible scale of loan losses. Back then, the unemployment rate surged from 6% to 11% and the underutilisation rate peaked at similar levels where it is now. Non-performing housing loans reached just under 2% of total loans in 1991, compared to 1.1% in Q2 2020.

"Two-thirds of homeowners own their house without a mortgage. So, if a similar share of homeowners were unable to service their loans as in 1991, that means that an additional 0.3% of homes would be at risk of forced sales. We estimate that this would be equivalent to around 30,000 homes today. If all of those homeowners were forced to sell their house over the coming year and listings surged accordingly, our sales-tolistings ratio would fall to around 0.9, consistent with house prices falling by around 2% per annum," he added.

"And new home sales have benefitted from the HomeBuilder grant, that payment is set to expire at the end of the year. We expect the border to remain closed for long-term migrants until mid-2021, which will keep a lid on population growth and housing demand.

"The closure of the border will continue to restrain demand for new homes. We expect the border to remain closed for long-term migrants until mid-2021, which means that demand for new housing will keep running around 50% below pre-virus levels for now," he continued.

"All told though, our previous forecast that house prices will keep falling until mid-2021 no longer looks fit for purpose. We now expect a smaller 3% peak to trough fall across the eight capital cities, with prices bottoming out by the end of this year and then rising by 7% in 2021. House prices in Melbourne may rise by a smaller 5%, while those in Sydney may increase by 10%. Rising house prices should support consumption growth and mean that dwellings investment may start to pick up again next year.

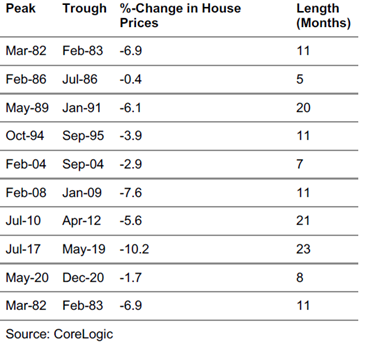

Eight Capital Cities Housing Downturns

Thieliant said a house prices rebound has implications for economic activity. Each 10% rise boosts consumption by around 1%, according to RBA estimates.

"While the speed of the recovery in household spending largely rests on the speed at which restrictions to prevent the virus from spreading are relaxed, wealth effects should still play some role. We expect consumption to bounce back by 5.5% in 2021 following an 8% slump this year.

"What's more, dwellings investment has on average reached a bottom two quarters after house prices started to rise. If our forecasts for house prices are correct, that meanshousing construction should start to recover in the second half of next year. That said, we suspect that following a 10% q/q plunge in Q3 due to the restrictions imposed on construction activity in Victoria, dwellings investment may already show signs of life by the end of this year. Indeed, we estimate dwellings investment to rise by 5% between the end of this year and end-2021." Thieliant concluded.

Westpac chief economist Bill Evans and senior economist Matthew Hassan were more optimistic, predicting prices could increase by around 15% over the next two years.

"We now expect many capital city markets to be more resilient with a national fall of 5% between April and June next year, distributed between: Melbourne (12%); Sydney (5%); Brisbane (2%); Perth (flat); and Adelaide (2%).

"Of most importance is that we are much more optimistic about the pace of price appreciation over the following two years with a total expected increase of around 15%," Evans and Hassan said.