Home >

Blog >

Australian Property Market Outlook Q2 2026

Australian Property Market Outlook Q2 2026

Posted

on 27 April 2026

Source: Australian Property Institute

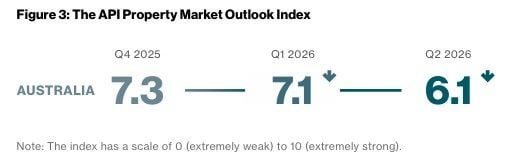

Property market momentum across Australia is expected to soften in Q2 2026, with the API Property Market Outlook Index sliding to 6.1 (from 7.1 in Q1 2026).

The property industry has become less optimistic (or more cautious) with all key asset classes. Residential is no longer the brightest spot, with market expectations showing more resilience for industrial.

The property industry is most cautious with office and retail, rating their outlook slightly below the neutral level.

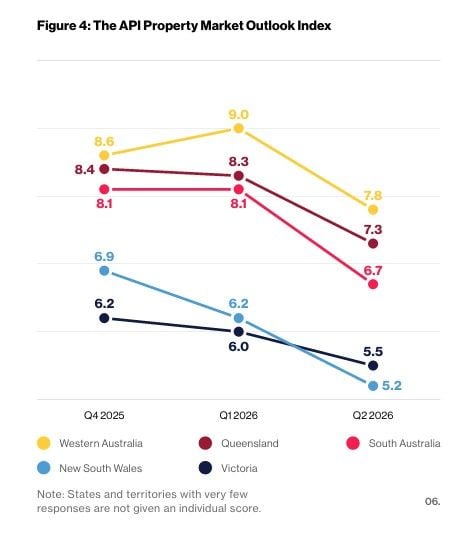

None of the five largest states is immune from the broad-based moderation in market sentiment. However, the overall property outlook remains positive, especially for Western Australia and Queensland.

Following the February and March cash rate hikes by the Reserve Bank of Australia—with the market anticipating more increases in the coming months—property valuers consider the interest rate outlook as the biggest source of downward pressure on property prices across the key asset classes in Q2 2026.

However, there are still factors sustaining or putting upward pressures on property prices such as:

the 5% Deposit Scheme, the continued population growth and insufficient housing supply (for residential)

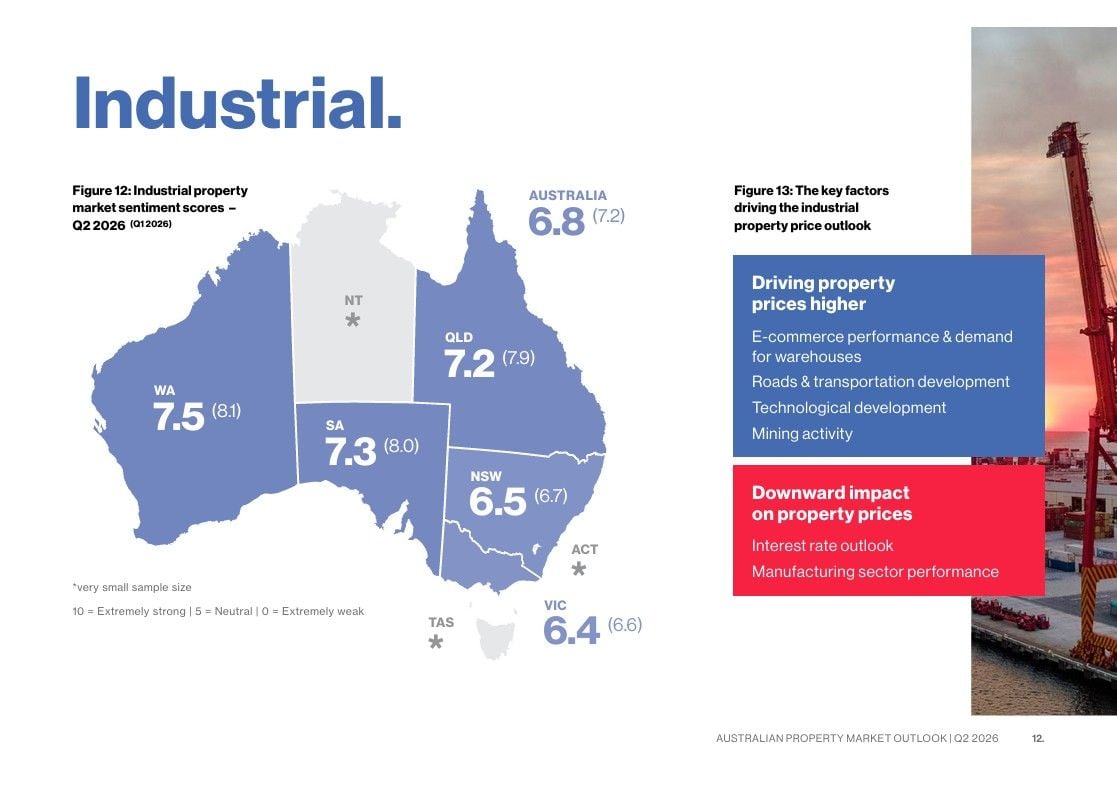

demand for warehouses and technological development (for industrial)

market demand for specific agricultural products (for agricultural).

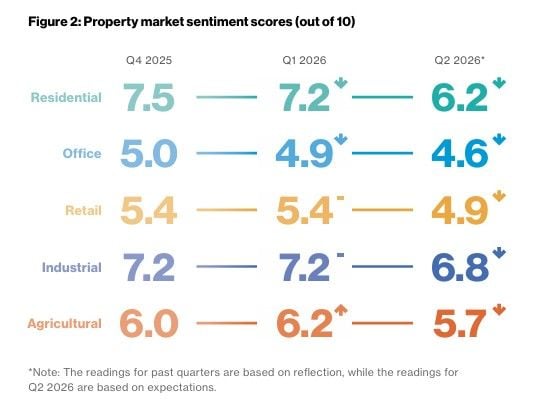

Property Market Sentiment.

The API Property Market Outlook Index fell to 6.1 (out of 10) for Q2 2026, with the five largest states all expected to experience a slowdown in property market momentum.

Nevertheless, the overall property market outlook remains positive for Western Australia, Queensland and South Australia, while the prospects for Victoria and New South Wales are near the neutral level (i.e. neither upbeat nor downbeat).

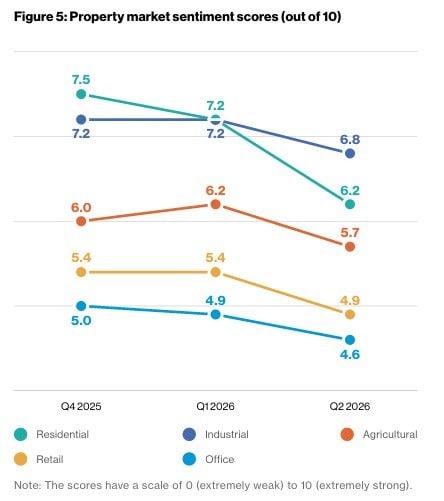

The breakdown of property market sentiment by asset class also shows an across-the-board moderation heading into Q2 2026.

Residential has the sharpest decline but remains the second-strongest and well within positive territory.

However, the readings for office and retail both come in below the neutral level, suggesting caution.

Property Price Outlook.

This section provides further insights on each of the core asset classes—residential, office, retail, industrial and agricultural.

Presented in this section are:

the breakdown of property market sentiment by state

the sources of upward or downward pressures on property prices, as identified by property valuers practising in the relevant sectors.